Today, it would be impossible to do anything without money for a few days, but before the industrial revolution, most people kept cattle and farmed their own food. They also tended to dwell in family homes that had been handed down through the centuries. As communities developed in size, most people were given money to spend on necessities such as food and lodging. Consumers in today’s capitalist society have access to a confusing array of both needed and non-essential items. Physical currency, electronic money, and legally binding contracts are examples of payment methods.

You do a lot more than just crunching numbers as an accountant, you develop a financial strategy, provide strategic counsel, stay up to date on tax legislation, take steps to save money for the client, increase revenue in their firm, and the list goes on. However, because accounting is a continually changing sector with many subcategories, you won’t be able to prosper if you stick to your old accounting skills. You must constantly study and expand your abilities to grow, innovate, and become a great accounting expert. Previously, only the wealthy were concerned with investing their money; now, money is now treated as a commodity, and all residents must be aware of its importance. The purpose of this blog is to give a quick overview of how accounting and finance play a part in society. There has always been trading between different tribes, and there is evidence of extensive trading in various implements in both the stone and bronze ages.

BACKGROUND (Brief History)

- FINANCE

The contributions of Markowitz, Tobin, Sharpe, Treynor, Black, and Scholes, to mention a few, helped to establish finance as a separate subject of theory and practice from economics in the 1940s and 1950s. However, many aspects of finance, such as banking, lending, investing, and money itself, has existed in some form or another since the dawn of civilization. Banking appears to have begun in the Babylonian/Sumerian empire around 3000 BC when temples and palaces were utilized as safe havens for financial assets such as grain, animals, and silver or copper ingots. In the country, grain was the chosen currency, while in the city, silver was preferred.

- ACCOUNTS

When it comes to early accounting history, Luca Pacioli can be the first name that comes to mind for people. In 1494, Pacioli published his “Summa de Arithmetica, Geometria, Proportions et Proportionalita,” which described double-entry accounting. While that can seem like a long time ago, accounting can have its origins even further back. Accounting has been practiced for millennia. It’s a necessary part of business, record-keeping, and daily life. Accounting began thousands of years ago in Mesopotamia and has since evolved into the complex aspect of business and society that it is today. Below is a helpful resource that takes you through a brief history of how accounting has changed over thousands of years. The first accounting documents were discovered among the ruins of Ancient Mesopotamia about 7,000 years ago. Accounting was used at the time to keep track of crop and livestock growth. Accountants must now follow accounting rules, auditing regulations, and ethical guidelines. Accountants and their peers are in charge of the economy’s monetary ebb and flow. Obviously, they are not the only ones to blame, but they play a significant role. Throughout their lives, every business, organization, corporation, government, and individual must employ at least basic accounting principles.

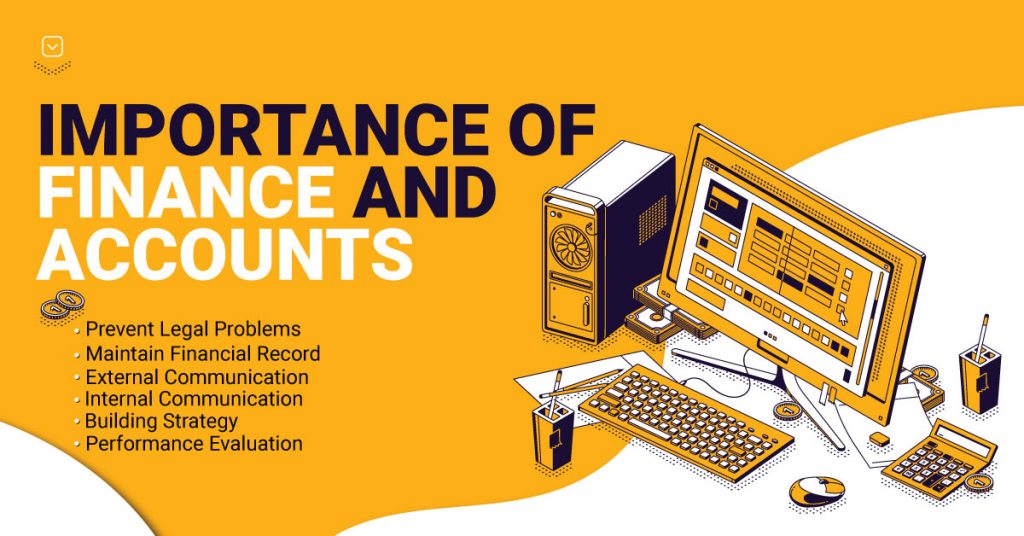

Importance of Finance and Accounts

Accounting, finance & understanding of your company’s numbers are critical to its success. The recording and analysis of company activities are referred to as accounting and finance. Understanding your incoming and outgoing cash flow will help you prevent failure by allowing you to make better decisions in the future. Accounting and financial management are critical for running a firm. There’s a considerable possibility you’ll lose control of your firm if you don’t know where your money is going and coming from. Businesses that manage their income and expenses have a better chance of growing. Furthermore, there is easier access to techniques that can guide in developing in surviving unexpected financial downturns.

Here’s how accounting and finances affect how you run your firm.

- Prevent Legal Problems

Keeping correct financial records aids in compliance with crucial corporate laws. A simple oversight could have a significant impact on your tax management. Financial managers must know what expenses can be deducted, how much tax must be paid, and when that tax must be paid. Poor financial records can result in an audit of your firm, putting you in unnecessary legal difficulties. Moreover, a financial overlook in facility upgrades could indicate that you are not sticking to safety regulations.

-

Maintain Financial Records

Accounting is a system for keeping track of a company’s financial transactions. A company’s ledger is where accountants and small business owners can keep track of a company’s daily activities’ income and expenses. An accurate financial statement can assist a company in managing its financial future and analyzing its cash

3. External Communication

When working with third parties, it is critical to communicate financial information. When applying for a bank loan or enticing potential investors, clear accounting and financial management might be beneficial. It is easier to give financial statements to external stakeholders when you have good financial management. These reports will be evaluated by external users to determine how they should proceed with their participation with your company.

- Internal Communication

Financial reporting can also aid in the communication of information among internal stakeholders. Employees interested in profit-sharing and stock-based pay can find this material useful. These records also enable owners to communicate their company’s strengths and faults to their employees. Allowing your employees to know your financial situation can be combined with a bonus structure that can be used to motivate production.

- Building Strategy

A good strategy closely leads to good accounting and financial management. After you’ve developed a budget and thoroughly reviewed your data, you should have a better grasp of how to construct a strategy to meet your bottom line. You will be better at making informed financial decisions on anything from staffing to supply management after evaluating your financial data. Your budget serves as a road map to your strategy, and strategy is the key to success.

- Performance Evaluation

Business owners who are successful are always looking in to see how their company is going. The historical and present records of obligations and assets, and other financial documents, can be used to assess a company’s financial status. This data can be used by a business owner to assess how well his or her firm is performing. These data provide an opportunity to learn from past failures and make better-informed judgments about future planning. Knowing your existing financial situation can also assist you in identifying new areas of expansion that will help you meet your goals.

SCOPE and FUTURE

While none of us can predict the future, we all have a responsibility to co

nsider and prepare for what is likely to occur. That requires working now to have the necessary people and technology in place in the finance function to take advantage of the impending upheaval. Without a clear vision and strategy for finance in a digital environment, this is unlikely to materialize. Now is the time to take a step back and double-check that your path to the future is clear.

Automation, cloud-based ERP, and cognitive innovations will continue to advance in the coming years, allowing businesses to streamline operations and free up personnel. The addition of blockchain to the mix will further speed up the trend. The capacity of humans to add value will be released as of this transformation advances.

Some people enjoy fantasizing about finance falling under the weight of technology transformation, but we don’t believe this will happen. Finance will most certainly be leaner, although that will mostly be due to manpower reductions in operational finance (order-to-cash, procure-to-pay, transactional accounting, etc.). Meanwhile, demand for corporate finance (such as joint ventures, reporting, planning, budgeting, and forecasting) and specialized finance (such as treasury, tax, and other services) will continue to rise. Accountants, for example, can use their distinctly human skills to translate high-quality data insights into more effective financial planning and reporting. They can engage with peers from different business units to use financial data to drive innovation, create more resilient and flexible supply chains, and establish business management plans that support growth while maintaining consistency in an interactive environment.

CFOs and accounting teams are being asked to be more strategic and creative. Top officials no longer need to waste their time on boring, repetitive tasks, especially given that there is a technology that reduces the need to complete financial and accounting transactions manually. Finance and accounting systems that have been in use for a long time are becoming obsolete. As a result, finance executives who continue to use slow, outdated technology that is inefficient and prone to human mistakes are putting their company in danger.

Outsourcing is a method that helps reduce operational expenses while obtaining the backing of top financial talent and the knowledge of skilled accounting experts, according to the future of finance and accounting. You can also take advantage of their cutting-edge digital finance solutions. Outsourcing your accounting to a Finance as a Service provider does not mean losing control. When done well, outsourcing includes adding a strategic partner who complements your existing financial staff and addresses operational gaps. You profit not only from their team’s skills and knowledge but also from their innovative technology, which is most likely cloud-based. As a result, corporate growth and flexibility have improved.

Clients are more demanding today, according to 82% of accountants, in terms of a greater range of services. Accounting technology has enhanced the productivity of 91% of accountants, and 83% of accountants feel that investing in the latest technology and digitization is important to keep up with the industry. (by Sage, 2020)

Accounting’s future will be influenced by technological advancements. To gain the benefits of quicker AI-powered operations, you will eventually have to say goodbye to your good old spreadsheet-based accounting methods. Despite the challenges of user acceptance, it is critical to keep up with the times by learning how to take advantage of new industry advances.

Advantages & Disadvantages of Finance and Accounts

Advantages of Financial Accounting

- Maintaining Financial Records

- Fraud Prevention and Detection

- Present true Financial Position

- Helps in preparing Financial Statements

- Comparison of Result

- Acts as Legal Evidence

- Assist the management

Disadvantages of Financial Accounting

- Records only Financial Aspects

- Historic in Nature

- Provides Incomplete Data

- No Cost Control Method

- Possibly Manipulated with Records Actual Cost

CONCLUSION

The future of finance and accounting does not include the removal of human workers and the replacement of every finance function with artificial intelligence and high automation. Rather, the finance professional’s position evolves, demanding new capabilities and learning requirements.

In the future of finance and accounting, human intervention in jobs that can be automated will be eliminated. Senior executives and human resources must be at the forefront of the shift, encouraging people to develop the skills and mentality required for financial transformation and the digital age. Businesses can make better decisions and scale quicker by embracing artificial intelligence, machine learning, robotic process automation, analytics, and other emerging technology.